In March and April of this year, the usually calm gold market became very active, breaking through its resistance level of $2,000 to $2,100, and increasing by $400 in just a few weeks. This surprised many people, especially Western investors and traders who had lost interest in gold and were more focused on the growth of tech stocks and cryptocurrencies.

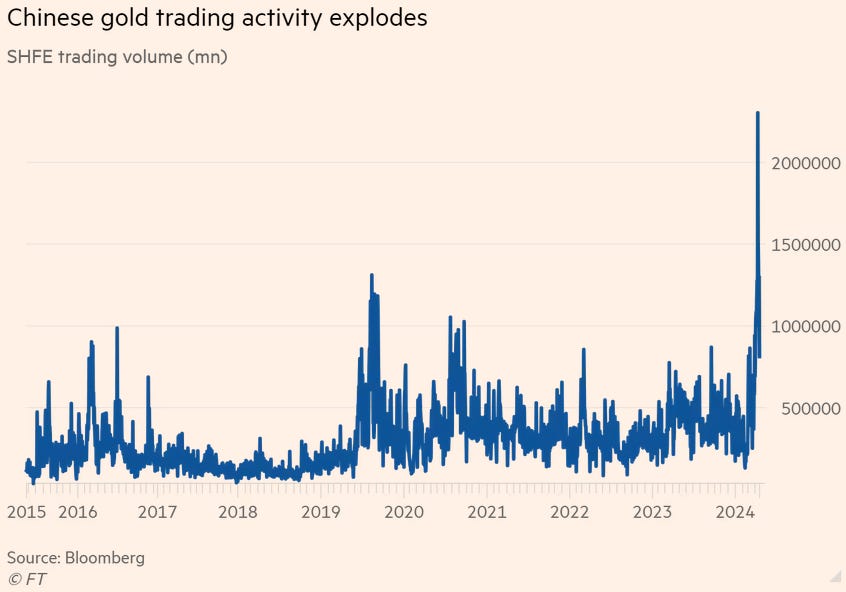

As gold’s rapid rise continued, more people began to wonder what was driving the surge. After some investigation, it was found that most of the excitement was coming from futures traders on China’s Shanghai Futures Exchange (SHFE) and the Shanghai Gold Exchange (SGE). A Financial Times article titled “Chinese Speculators Super-Charge Gold Rally” highlighted how trading volume in SHFE gold futures went up by 400%, pushing gold prices to record levels:

More proof of the gold trading boom in China can be seen in the chart showing the rise in SHFE gold futures:

This situation showed that the East was having more influence on the gold market, while the West was starting to take a back seat.

As the World Gold Council’s chief market strategist, John Reade, said in the Financial Times:

“Chinese speculators have really grabbed gold by the throat.”

“Emerging markets have been the biggest end consumers for decades but they haven’t been able to exert pricing power because of fast money in the West. Now, we are getting to the stage where speculative money in emerging markets can exert pricing power.”

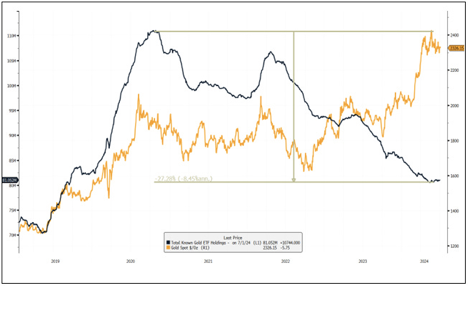

While Chinese traders and investors were driving up the gold market, Americans had been selling their gold-related assets for over three years. This can be seen in the black line on the chart showing total gold holdings in U.S. exchange-traded funds (ETFs):

There are two main reasons why Americans have been selling gold-related assets in recent years:

- High real interest rates

- Low financial fear/high financial confidence

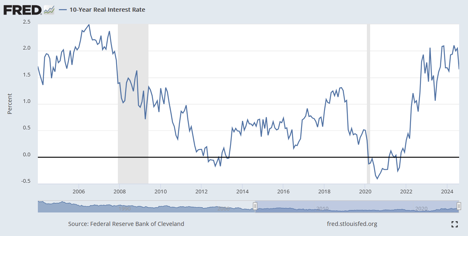

As shown in the chart below, the 10-year U.S. real interest rate (adjusted for inflation) has been close to a 20-year high. Unlike stocks, bonds, or real estate, gold and silver don’t generate any income. When inflation-adjusted interest rates are high, investors prefer higher-yielding assets like savings accounts, money market funds, certificates of deposit, bonds, and dividend-paying stocks.

When these real interest rates are high, holding assets like gold and silver, which don’t produce income, seems less attractive. On the other hand, when real interest rates are low or negative, as they were in the early 2010s and again in 2020–2021, people are more likely to buy gold and silver.

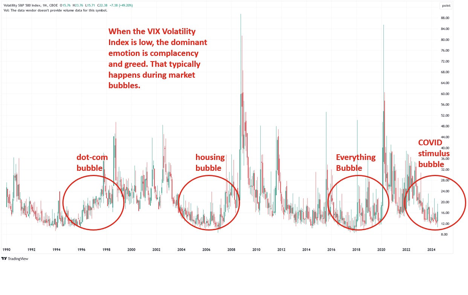

In the U.S., gold is often seen as a “fear asset,” linked with survivalists who stock up on items like guns, ammo, and canned goods. Because of this, demand for gold rises during recessions, financial crises, and times of inflation, but falls during times of low financial stress and a booming stock market.

As the chart of the S&P 500 Volatility Index shows, U.S. stock market investors were not very worried during 2023 and early 2024, which explains their lack of interest in safe-haven assets like gold. U.S. investors also ignored gold during other market bubbles, such as the late-1990s dot-com bubble, the mid-2000s housing bubble, and the late-2010s “Everything Bubble”—all of which turned out to be good times to buy gold at low prices before big rallies.

While the U.S. economy and stock market were lifted by trillions of dollars in COVID stimulus, China’s economy has been going through one of its worst downturns in decades. China’s once-thriving stock and property markets peaked in 2021 and have been in a steady decline similar to Japan’s market crash in the early 1990s. China’s property market crash has been so severe that its real estate billionaires have already lost $100 billion in just a few years. Unfortunately, China’s economic problems don’t seem to be ending anytime soon.

The SSE Composite Index—China’s main stock index—has dropped sharply in the past few years and is sinking again after a brief rise in early 2024:

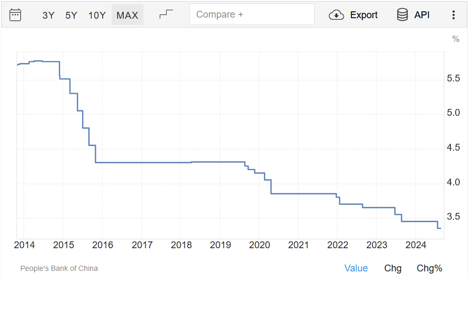

In response to this economic downturn, the People’s Bank of China lowered interest rates to record lows:

China’s low interest rates are very different from the U.S. rates, which are at their highest since the 2008 financial crisis. Since gold, a non-yielding asset, does better in low-interest rate environments, this explains why Chinese traders and investors have been driving up gold prices while American investors have been selling it.

In early 2024, many Chinese investors became frustrated with their falling stock and property markets and began turning to gold. Chinese retail investors started flocking to buy gold bullion, including small “gold beans” that sold for 600 yuan, or about $83 each.

This gold-buying frenzy in China lasted from mid-February to mid-April, until it suddenly stopped. Several factors caused this, including tighter trading rules and limits from the Shanghai Futures Exchange and Shanghai Gold Exchange, as well as high gold prices reducing demand from Chinese and Indian buyers.

Since mid-April, gold prices (in U.S. dollars) have been slowly trending upward, with several attempts to reach new highs but pulling back each time:

While investors like me appreciate the gains in gold prices, many people have expressed disappointment over the rally’s lack of strength in the past few months.

On social media, I’ve seen comments like:

“Gold and silver are due for a crash any day now!” “Gold and silver MUST correct first before rising any further.” “Why do gold and silver go two steps forward and one step back?” “Why is silver struggling?” “Why are gold mining stocks lagging behind?”

One reason for gold’s slow progress is that the gains have mostly been driven by a weak U.S. dollar, not by gold’s own strength. Gold and the U.S. dollar usually move in opposite directions—when the dollar weakens, gold rises, and vice versa.

Since late April, the U.S. Dollar Index has been on a downward trend:

Interestingly, despite gold’s recent gains in U.S. dollars, its price has barely moved in Chinese yuan and other major currencies. That’s why gold’s summer rally has been weak—it hasn’t been growing strongly across all currencies! Please keep this in mind next time you feel tempted to complain about gold’s performance.

The chart below shows Shanghai Futures Exchange gold futures, which led the gold frenzy in March and April. Since the April peak, prices have stayed within a set range.

Here’s my theory and the main point: if SHFE gold futures break above the 585 resistance level (or 18,000 in the XAUCNY spot) with strong volume, it’s likely that Chinese gold traders will jump back in, pushing gold much higher like they did in March and April.

Once SHFE gold futures go past 585, automated buy programs will kick in, traders will fear missing out, and the rest of the world will join in as well. Also, China’s ongoing economic problems—and soon the United States’—should keep demand for physical gold strong in the years ahead.

Although gold buyers in China and India have slowed down due to high prices, they will eventually realize that prices probably won’t drop anytime soon. This could cause a rush to buy gold before prices go up even more.

If SHFE gold breaks out of its range, we might see what’s called a “measured move,” where a rally is expected to rise by the same amount as the increase that came before it. By this logic, gold could reach about $3,000 just a couple of months after breaking out! This isn’t as crazy as it sounds—that’s only a 20% increase from where we are now, which has already happened this year.

Remember, though, this idea depends on a strong breakout. Without that, things could go differently. Also, keep in mind that gold might briefly pull back before it finally breaks out.

In conclusion, Chinese gold futures traders drove the big $400 rally in gold earlier this year. Since April, those traders have been quiet, causing gold prices to stall, especially when priced in non-U.S. currencies. But this is actually something to be optimistic about. There’s a good chance that when gold breaks out of its current range, those same Chinese traders could ignite another big rally, with the rest of the world joining in to push gold toward $3,000.

Ref: https://goldseek.com/article/why-chinese-traders-may-soon-propel-gold-3000